It will go from the current six million to fourteen, with photovoltaic, wind, electric vehicles and heat pumps at the forefront. The global market for major mass-produced clean energy technologies will also grow, reaching a value of up to $650 billion annually by 2030. China has the largest manufacturing capacity announced through 2030 in photovoltaic, wind, and electric vehicle batteries; the Republic of the Congo alone produces 70% of the world’s cobalt; and only 3 countries concentrate more than 90% of the world’s lithium production. These are some of the keys to the Energy Technology Outlook for 2023, the latest report from the International Energy Agency.

Jobs related to manufacturing will more than double, reaching almost fourteen million in 2030. Or what is the same, in the next seven years renewable energies will create eight million jobs worldwide (currently there are six million), with more than half of them related to electric vehicles, photovoltaic solar energy, wind energy and heat pumps. But employment will not be the only sector that grows. The global market for major mass-produced clean energy technologies will triple in value today, meaning it will be worth about $650 billion annually by 2030.

But all this if the following condition is met: “that countries around the world fully comply with the commitments announced in the field of energy and climate”. These are two of the main conclusions of the International Energy Agency in its latest report published ‘Perspectives of energy technology for 2023’ which is, in turn, the first world guide on renewable energy industries. The following lines show a summary of what this report offers in terms of analysis of global manufacturing of solar panels, wind turbines, batteries for electric vehicles, hydrogen electrolyzers and heat pumps, as well as their supply chains around the world and the evolution of all this in the coming years.

The three largest countries that produce solar panels, wind turbines, batteries for electric vehicles, electrolysers and heat pumps concentrate at least 70% of the manufacturing capacity of each technology . China has the largest manufacturing capacity announced to 2030 in solar PV (about 85% for cells and modules, and 90% for wafers), wind (about 85% for blades, and about 90% for nacelles and towers). ) and electric vehicle batteries (98% for anodes and 93% for cathode material). These data reflect the current situation of supply chains and the risks they present due to the high geographic concentrations in terms of technology manufacturing, but also in the extraction and processing of resources.The main exception is hydrogen electrolysers with around a quarter of manufacturing capacity announcements by 2030 in China and the European Union , respectively, and another 10% in the United States. A tension in the supply chains that have caused the prices of renewable technologies to rise in recent years, making it difficult and more expensive for countries to transition to clean energy. Rising prices for cobalt, lithium and nickel led to the first rise in prices for electric vehicle batteries, which rose nearly 10% globally by 2022. The cost of wind turbines outside of China it has also increased after years of declines, and similar trends are observed in solar PV.

[Below these lines, graph on employment in the global energy sector by technology in the Net Zero scenario]

Fatih Birol, IEA Executive Director: “The IEA highlighted almost two years ago that a new global energy economy was rapidly emerging. Today, it has become a central pillar of economic strategy and each country needs to identify how it can benefit from the opportunities and navigate the challenges. We are talking about hundreds of billions of dollars worth of new markets for renewable technologies, as well as millions of new jobs.The encouraging news is that the global pipeline of projects for manufacturing renewable energy technologies is large and If everything announced today were built, investment in manufacturing clean energy technologies would provide two-thirds of what is needed to achieve net-zero emissions.”

As for renewable energy projects, “with relatively short terms of between 1 and 3 years on average”, they leave data such as that only 25% of the photovoltaic solar energy manufacturing projects announced worldwide are being built or construction will begin imminently . The figure is around 35% in the case of batteries for electric vehicles and less than 10% in the case of electrolyzers. The percentage is higher in China, where 25% of the total manufacture of photovoltaic solar energy and 45% of the manufacture of batteries are already in an advanced phase of execution. In the United States and Europe, less than 20% of announced battery and electrolyzer factories are under construction.

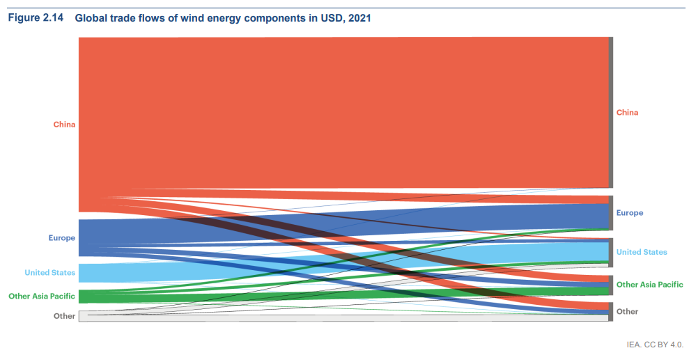

The ETP-2023 report also underlines the important role of international trade in the supply chains of clean energy technologies. The share of international trade in global demand is nearly 60% for solar PV modules , and about half of the solar modules made in China are exported, mostly to Europe and the Asia-Pacific region. . Electric vehicle batteries and wind turbine components also have China as the top net exporter at present, exporting around 25% and 30% respectively. “International trade is vital to achieving fast and affordable clean energy transitions, but countries need to increase supplier diversity,” the IEA adds.

Fatih Birol, IEA Executive Director: “The current momentum is bringing us closer to meeting our global energy and climate goals, with more to come. At the same time, the world would benefit from more diversified cleantech supply chains. As we have seen with Europe’s reliance on Russian gas, when you become too dependent on one company, one country, or one trade route, you risk paying a heavy price in the event of disruption.So I am pleased to see many economies in Today, around the world are competing to lead the new energy economy and fuel an expansion of cleantech manufacturing in the race to net-zero energy, it is important, however, that this competition is fair and that there is a healthy degree of international collaboration. ,since no country is an energy island and energy transitions will be more expensive and slower if countries do not work together”

Manufacturing projects announced through 2030 are very large for many clean energy technologies. If all the announced projects to expand manufacturing capacities materialize and all countries meet their announced climate commitments, “China alone could supply the entire world market for photovoltaic solar modules by 2030, a third of the world market for electrolysers and the 90% of the world’s electric vehicle batteries”, continues the IEA. The projects announced in the European Union would be enough to supply all the national needs for electrolysers and batteries for electric vehicles, but it would still depend heavily on imports of solar photovoltaic and wind energy. The situation is somewhat similar in the United States, although it is very likely that further capacity expansions will take place as a result of the Reduction of Inflation Act. The current global portfolio of announced projects would exceed the demand for some technologies (solar photovoltaics, batteries and electrolysers) and would fall far short in the case of others (wind components, heat pumps and fuel cells).

Solar PV:

Module manufacturing capacity is already well above current demand, with a global average utilization rate of less than 50% by 2021. Announced expansion plans would bring capacity to around 790 GW by 2027, enough to cover all demand forecast for 2030 in the Net Zero Scenario . The situation for cell manufacturing is almost identical, with expansion plans announced that will increase global manufacturing capacity to around 810 GW by 2027, enough to meet projected demand in 2030. Wafers are also on track, with a margin Similar to cells and modules: if all projects are completed on time, manufacturing capacity would reach over 790 GW by 2027.

[Below these lines, graph reflecting global trade flows along the solar PV supply chain, 2021]

Wind:

Like photovoltaic solar energy, the deployment of wind energy has been a great success. Led mainly by the construction of onshore wind farms, the global deployment of wind turbines around the world has increased almost twenty-fold since the year 2000, when developers installed only about 5 GW of generation capacity and European companies supplied 90% of the market. Global installed wind generation capacity reached about 830 GW in 2021, providing almost a quarter of the world’s renewable electricity, second only to hydropower. Thanks to the realization of economies of scale, technological innovation, and strong political support for clean energy technologies, wind is now among the most affordable options for new generation capacity worldwide. Chinese manufacturers have supplied up to 40% of the equipment used in deployed capacity to date.

Currently, manufacturers of onshore and offshore wind components are increasing their capacity at a slower rate than required in the NZE scenario, which projects global wind turbine deployment to quadruple between 2021 and 2030, with a capacity of about 315 GW onshore and about 85 GW offshore. The announced expansion plans would increase the manufacturing capacity of land blades by only 11%, to around 110 GW in 2030. In the case of land nacelles, manufacturing capacity would grow by around 8%, up to 108 GW, while that that of the terrestrial towers would be increased by only 5%, up to 92 GW. The picture is similar for offshore wind components. Manufacturers have announced capacity increases of 55% for offshore towers, 31% for blades and 21% for nacelles, but these increases remain well below what is needed by 2030 in the NZE scenario (Figure 4.6).

[Below these lines, graph on global trade flows of wind energy components, 2021]

Electrolyzers for hydrogen:

According to company announcements, the manufacturing capacity of electrolyzers will increase tenfold to reach more than 100 GW per year in 2030, accompanied by a similar expansion of component manufacturing capacity. However, this impressive growth, even if fully realized, would still be insufficient to meet the expected growth in electrolyser demand in the near term in the NZE Scenario, as it would only cover about half of the 200 GW annual capacity. manufacturing capacity needed by 2030. Furthermore, only about 8% of the announced expansion of electrolyser manufacturing capacity has reached the final investment decision. Both government targets and industry plans to invest in electrolyser installation also fall short of the planned deployment in the NZE Scenario, where more than 700 GW of electrolysis capacity is installed by 2030 (IEA, 2022e). Governments’ global targets call for capacity of just 145-190 GW, while projects currently under development, if completed in full and on time, would result in 240 GW of capacity by then. then.

Currently, electrolyser manufacturing is highly concentrated in China and Europe, which account for two-thirds of the world’s manufacturing capacity. Although these two regions are expected to maintain a prominent role in electrolyser manufacturing, their shares are expected to fall to around 25% each by 2030 (although this drop may be less pronounced, as one fifth of expansions announced have not yet been allocated specific locations and some of this capability could be deployed in Europe and China). Regions that currently have no manufacturing capacity in place and expect to deploy new capacity include the Middle East, where more than 1% of global manufacturing capacity is expected to be installed by 2030, and Australia, where a factory is expected to be built. give the country a 2% quota.

Heat pumps:

Manufacturing capacity will grow in the coming years, but it is not known with certainty at what rate, since few expansion projects are announced or advertised. Global heat pump manufacturing capacity would need to nearly quadruple to around 460 GWth by 2030 to meet projected demand in the NZE scenario. Currently, China, Japan and Korea are net exporters of heat pumps, while North America and Europe are net importers. Several countries are implementing policies to increase domestic manufacturing, and several new companies are entering the heat pump market to meet the growing demand. In general, heat pump manufacturing capacity is evenly distributed geographically and the market is less concentrated than most other mass-produced clean energies. This is not expected to change much before 2030, based on current trends and investment plans. North and East Asian companies are expected to remain the largest producers, but significant capacity growth is expected in Europe and North America.

Some conclusions

• Holistic assessment and promotion of these competitive advantages should be a central pillar of governments’ industrial strategies, designed in accordance with international standards and complemented by strategic partnerships.

• Energy costs will continue to be an important differentiating factor in the competitiveness of countries’ energy-intensive industrial sectors. For example, the costs of producing hydrogen from renewable electricity could be much lower in China and the United States (3-4 USD/kg) than in Japan and Western Europe (5-7 USD/kg) using the best resources. of those countries today, which would translate into similar differences in the production costs of derivative products such as ammonia and steel.

• The new infrastructures will constitute the backbone of the new energy economy in all countries. This covers areas such as the transport, transmission, distribution or storage of electricity, hydrogen and CO2.

• Each country has a different starting point and different strengths, so each country will have to develop its own industrial strategy for manufacturing clean energy technologies. And no country can do it alone. As countries develop their national capabilities and consolidate their position in the new global energy economy, international cooperation can bring enormous benefits in efforts to build a solid foundation for the industries of the future.

Source: Renewable Energies (2023)